What is the District Heating Market Overview – definition, scope, and significance?

District heating is a centralized system that produces thermal energy at a plant and distributes hot water or steam through insulated pipelines to multiple end‑users for space heating, water heating, and industrial processes. The market encompasses all plant types—boilers, combined heat and power (CHP) units—and a range of heat sources such as coal, natural gas, and oil. Its significance lies in improving energy efficiency, reducing carbon emissions, and supporting urban sustainability goals, especially as cities seek low‑carbon heating solutions.

What are the District Heating Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include growing urbanization, stricter environmental regulations, and the economic advantage of shared infrastructure. Restraints stem from high upfront capital costs and legacy fossil‑fuel dominance in some regions. Major challenges involve integrating renewable heat sources, navigating complex permitting processes, and maintaining pipeline integrity over long distances. Opportunities arise from digitalization of network management, expanding CHP applications, and policy incentives that favor low‑carbon heat generation, creating a fertile environment for innovative business models.

What are the current District Heating Market Growth Trends?

Trend analysis shows a shift toward CHP plants that combine electricity generation with heat, enhancing overall efficiency. Renewable heat integration—particularly biomass and waste‑to‑energy—gains momentum, driven by decarbonization targets. Smart metering and IoT‑based monitoring are being deployed to optimize distribution losses and demand response. Additionally, public‑private partnerships are increasingly used to finance large‑scale projects, while modular plant designs enable faster deployment in emerging urban zones.

How has COVID‑19 impacted the District Heating Market and what is the recovery trajectory?

The pandemic temporarily slowed new project approvals due to disrupted supply chains and delayed financing. However, essential heating services remained operational, preserving revenue streams for existing operators. Post‑2020, governments accelerated clean‑energy stimulus packages, revitalizing investment in district heating upgrades. Recovery is now on a steady upward path, with the market projected to resume robust growth as urban rebuilding efforts prioritize resilient and low‑carbon heating infrastructure.

What does the District Heating Market Competitive Landscape look like and how is consolidation shaping the sector?

The sector is characterized by a mix of large multinational engineering firms and specialist heat‑service companies. Major players such as Siemens AG, Engie SA, and Veolia dominate equipment supply and network operations, while firms like Danfoss AS and LOGSTOR focus on control systems and storage solutions. Recent years have seen strategic acquisitions—particularly of smaller CHP technology firms—aimed at expanding service portfolios and geographic reach, indicating a moderate consolidation trend toward integrated solution providers.

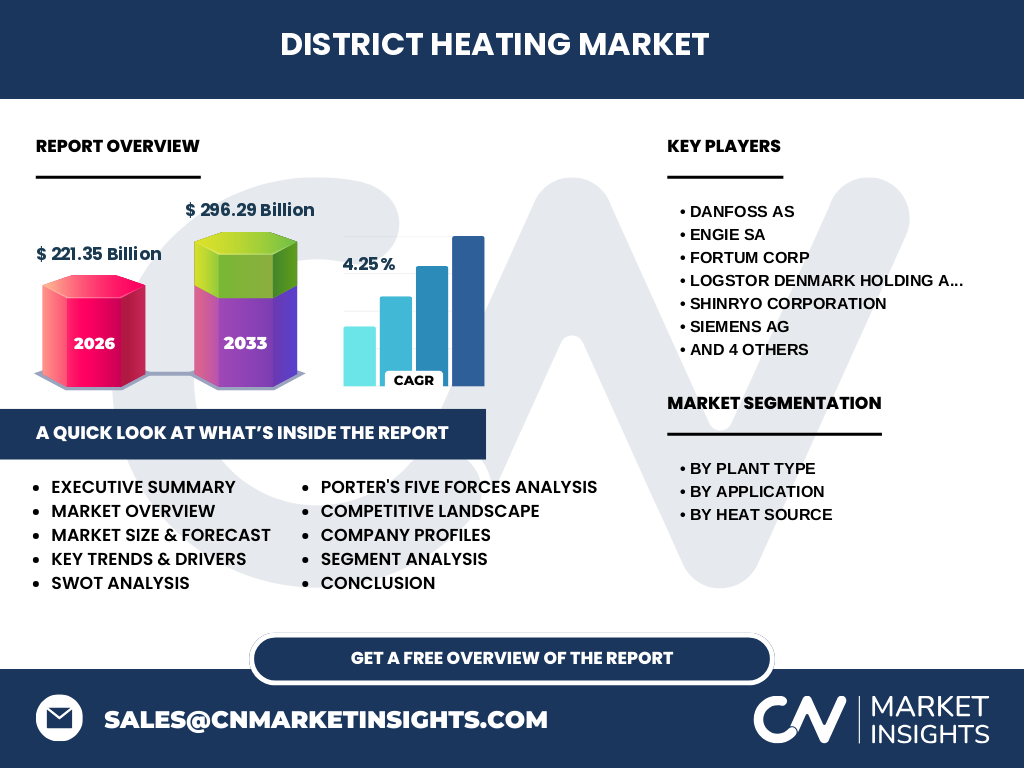

What are the key findings in the Executive Summary of the District Heating Market?

The market is valued at $221.35 billion in 2026 and is forecast to reach $296.29 billion by 2033, reflecting a 4.25 % CAGR. Growth is driven by urbanization, sustainability mandates, and the efficiency advantages of CHP. While capital intensity and legacy fuel dependence pose constraints, digitalization, renewable integration, and supportive policy frameworks present strong upside potential. Leading firms are leveraging mergers, advanced controls, and modular designs to capture emerging opportunities across residential, commercial, and industrial segments.

What are the District Heating Market Forecast expectations for 2025‑2032?

Based on the given CAGR of 4.25 %, the market is expected to maintain a steady upward trajectory through 2032, expanding well beyond the 2027 estimate of $296.29 billion. Incremental growth will be fueled by expanding CHP capacity, increasing adoption of natural‑gas‑based plants, and the gradual replacement of coal‑driven systems with cleaner alternatives. Emerging economies with rapid urban growth will contribute significantly, while mature markets will focus on network optimization and renewable heat integration.

How is the District Heating Market Size and Share broken down by segmentation?

Segmentation by plant type divides the market into boiler‑based systems and combined heat and power (CHP) units, with CHP gaining a larger share due to its dual‑output efficiency. By application, residential use accounts for the bulk of demand, followed by commercial and industrial users, each requiring tailored temperature profiles and reliability levels. Heat source segmentation includes coal, natural gas, and oil‑based fuels; natural gas is increasingly favored for its lower emissions, while coal retains a presence in regions with abundant supplies and legacy infrastructure.

What is the Global District Heating Market Size and Share by Region?

The market spans North America, Europe, Asia‑Pacific, and Rest of World, with Europe historically holding the largest share because of extensive district networks in Scandinavia and Central Europe. Asia‑Pacific is emerging rapidly, driven by China’s aggressive urban heating programs and Japan’s post‑disaster reconstruction efforts. North America shows moderate growth, primarily in the Northeastern United States and Canadian provinces, while the Rest of World includes developing regions where pilot projects are establishing the market foundation.

What does the Regional Analysis of the District Heating Market reveal?

European nations such as Denmark, Sweden, and Germany demonstrate mature networks, high efficiency standards, and strong policy support, resulting in stable revenue streams. In Asia‑Pacific, China’s central heating mandates for northern cities and Japan’s focus on resilient infrastructure after 2011 are accelerating installations. North America’s growth is anchored in retrofitting older district systems and integrating renewable heat sources. Latin America and the Middle East are at nascent stages, with strategic investments expected as urban populations expand.

Which companies lead the District Heating Market and what are their core strategies?

Key leaders include Danfoss AS, which emphasizes advanced control and valve technologies; Engie SA and Veolia, focusing on end‑to‑end network operation and renewable heat contracts; Fortum Corp and Statkraft AS, leveraging their renewable generation assets to supply heat; Siemens AG, providing digital automation and turbine solutions; LOGSTOR Denmark Holding ApS, specializing in thermal storage; Shinryo Corporation, expanding in the Japanese market; Vattenfall AB, pursuing carbon‑neutral heating; and Vital Energi Ltd, integrating offshore wind heat conversion. Their strategies converge on digitalization, sustainability, and expanding service portfolios.

How does Porter’s Five Forces analysis apply to the District Heating Market?

Threat of new entrants is moderate due to high capital requirements and regulatory barriers. Bargaining power of suppliers is limited because many components are commoditized, though specialist equipment providers retain some leverage. Bargaining power of buyers is low for municipal clients but higher for large commercial/industrial users seeking tailored contracts. Threat of substitutes is modest, with electric heat pumps and individual boilers posing competition, yet district systems retain efficiency advantages. Industry rivalry is intense, driven by a few dominant global players competing on technology, service reliability, and financing solutions.

What are the SWOT insights for the District Heating Market?

Strengths: High energy‑use efficiency, lower per‑unit emissions, and long‑term cost stability. Weaknesses: Significant upfront investment and reliance on existing fossil‑fuel infrastructure in some regions. Opportunities: Integration of renewable heat sources, digital network optimization, and supportive climate policies. Threats: Competition from decentralized electric heating, regulatory delays, and potential fuel price volatility for coal and oil‑based plants.

What does the District Heating Market Value Chain look like?

The value chain begins with fuel procurement (coal, natural gas, oil) and proceeds to heat generation via boiler or CHP plants. Energy is then transferred to a distribution network managed by utilities or specialized operators, incorporating thermal storage where applicable. End‑users receive heat through consumer‑side connections and metering. Supporting services include engineering, construction, equipment supply (valves, turbines, controls), and digital monitoring platforms that provide data for maintenance and demand management.

What key investment insights can be drawn for the District Heating Market?

Investors should prioritize projects that combine CHP technology with renewable fuel blends, as these offer superior returns on efficiency and regulatory incentives. Funding modular plant designs reduces construction risk and accelerates deployment. Equity participation in established network operators provides stable cash flows, while venture capital in IoT‑based optimization startups can capture upside from digital transformation. Geographic focus on Europe’s mature markets and Asia‑Pacific’s fast‑growing cities can balance risk and growth potential.

What are the main conclusions of the District Heating Market study?

The district heating sector is on a clear growth path, underpinned by urbanization, climate targets, and efficiency imperatives. While capital intensity and legacy fuels present hurdles, the market’s resilience—demonstrated during the COVID‑19 shock—combined with emerging digital and renewable technologies creates a compelling investment narrative. Stakeholders that align with policy trends, adopt modular and low‑carbon solutions, and leverage data‑driven operations will likely lead the next decade of expansion.

How was the research methodology designed for this District Heating Market report?

The study employed a mixed‑method approach, combining primary interviews with industry executives, technology providers, and municipal officials, alongside secondary data from company filings, government publications, and reputable market databases. Trend extrapolation used the provided CAGR of 4.25 % to forecast revenue. Qualitative assessments such as Porter’s Five Forces and SWOT were derived from expert insights and cross‑checked against peer‑reviewed literature to ensure robustness.

What is the defined research scope for this District Heating Market analysis?

The scope covers global district heating activities, segmented by plant type (boiler, CHP), application (residential, commercial, industrial), and heat source (coal, natural gas, oil). Geographic coverage includes all major regions, with emphasis on Europe, Asia‑Pacific, and North America. The analysis excludes unrelated thermal services such as standalone residential boilers and focuses on centralized distribution networks. Timeframe extends from the base year 2026 through the forecast horizon of 2033.

Which key companies are highlighted and what recent developments have they announced?

Leading firms include Danfoss AS (launch of AI‑enabled valve controls), Engie SA (agreement to retrofit 15 MW of coal‑based plants with biomass), Fortum Corp (investment in geothermal heat projects in Finland), LOGSTOR Denmark Holding ApS (deployment of large‑scale thermal storage units), Shinryo Corporation (partnership with local governments for district heating expansion), Siemens AG (release of a digital twin platform for network optimization), Statkraft AS (integration of offshore wind‑derived heat), Vattenfall AB (commitment to carbon‑neutral heating by 2030), Veolia (acquisition of a regional network in France), and Vital Energi Ltd (pilot of hybrid CHP‑solar thermal systems). These moves illustrate a clear shift toward digitalization, renewable integration, and strategic expansion.